Blog Post

The Current State of Core Insurance Technology Part 6: Core System Modernization

In this series, we share insights from a recent study* which seeks to understand the current state of core insurance systems and market sentiment for adopting SaaS-based models.

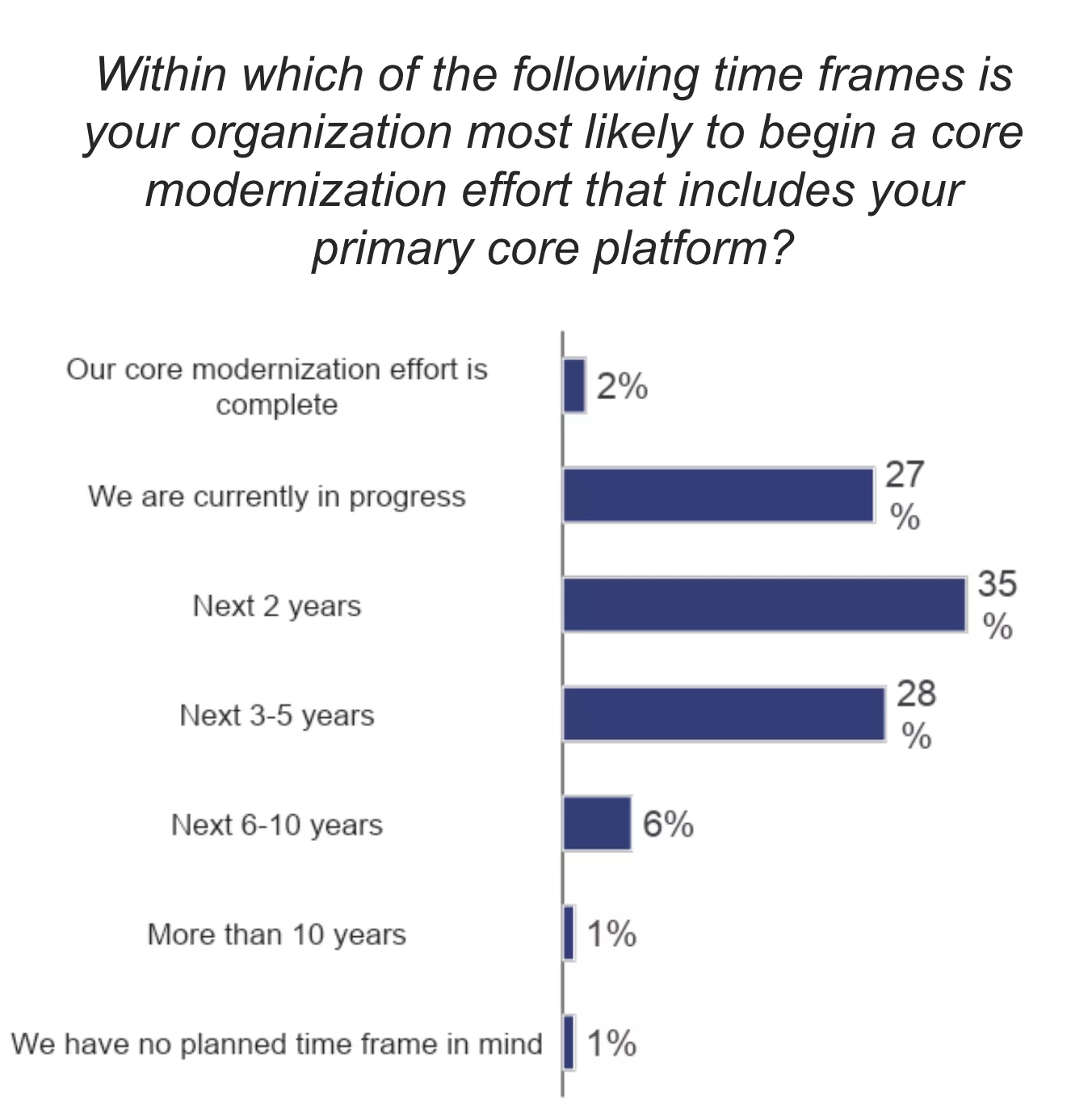

Given the disproportionately higher number of responses indicating lower confidence in the ability of on-premises and private cloud systems to adequately enable digital transformation, we asked a follow-up question to better understand timelines around such moves.

Just shy of one-third of respondents disclosed they were currently in the process of core modernization. Another 63% intend to start the process within the next five years. Combined, those currently undergoing, and those planning to transform in the short term represent 90% of total responses.

While challenges to modernization efforts fluctuate over the buying and implementation cycle, in the aggregate, the complexity that comes from managing multiple systems poses the greatest issue (59%). However, different trends emerge when the data is analyzed more granularly. For example, 57% of those anticipating beginning their core modernization efforts in the next two years cited the cost of modernization as the greatest challenge, compared to only 44% on average. Interestingly, for those already underway with their efforts, the top cited challenge was predominately the complexity of the project, coming in at 72%.

Core transformations are naturally complex. They are, after all, expected to run the daily underwriting, billing, and claims operations with their respective security, communication, automation, and integrations and deliver exceptional business outcomes. It’s, therefore, a balancing act to vet vendors who not only are able to lay out a roadmap of expectations intended to keep the project on track and within budget, but also select a platform that increases the likelihood of implementation success.

To learn more about why the architecture matters for selecting core insurance cloud technology, download our eBook.

*Research Methodology and Respondent Profile

This research was commissioned by Origami Risk and conducted by Arizent/Digital Insurance between September 22 and October 20, 2022, among 100 qualified respondents. To qualify, insurance industry professionals had to have a management role (in a non-legal/HR function) and have knowledge of their organization’s core systems or primary supporting services.

51% of respondents self-identified as P&C insurance carriers, 25% as insurance brokers/agents, 12% as MGA/MGU, and 12% as third-party administrators.

Total Respondents: n=100; Annual premiums under $1B: n=35/Annual premiums of $1B or more: n=65; IT/technology role: n=16; Primary core system is all or mostly on-premises: n=26; Senior business unit executive: n=28/Division or dept head/director: n=36.